Salomon-Arc'teryx Playbook and IPO

Salomon-Arc'teryx Playbook and IPO

4 min read @ 1001 words

SALOMON-ARC’TERYX-WILSON PARENT OPENS UP THEIR PLAYBOOK FOR IPO (sec filing)

Amer Sports, parent company of Salomon, Arc’teryx, Wilson and a collection of other brands has filed papers to go public on the NYSE. The company plans to list under the stock symbol “AS”.

The company has been on a revenue hot streak with Arc’teryx and Salomon fueling 30% growth in the first nine months of 2023 vs the same period in 2022. Gross margins are up 260 basis points to 52.2% as are net losses at $253M (2022). Owned retail door count at 330 with aggressive investment in Greater China and more planned.

This is not new news as multiple media outlets have covered the topic and filtered the IPO filing to varying degrees for their audience. Footwear Insider loves to dig and went full-nerd on the 200+ page document. We’ve broken down our findings into digestible chunks and will share over multiple posts.

Current ownership:

Amer Sports was acquired in 2019 by China’s Anta Sports and a group of investors that include Tencent Holdings and Lululemon Founder Chip Wilson’s investment company Anamered Investments, Inc

Aquisition price: $5.2B

IPO details and scale amongst peers:

According to Bloomberg, the deal could raise up to $1B at a valuation around $10B.

A $10B valuation would put them in the same neighborhood as Birkenstock, On and Skechers. Prior to their 41% drop in market cap over the past year, VF Corp (Vans, TNF, Supreme, Timberland) was in the same $10B-ish financial zip code.

Pardon corporate-looking Keynote slides in this week’s post. This represents 17-yrs of Nike muscle-memory and lessons on how to communicate with other corporate humans. Did I get the font the right? I’m claiming ignorance if the template police are pissed I broke protocol.

Amer Sports Transformation

Brand-direct operating model. Provides “significant autonomy” on strategy, product innovation, design and development, marketing, sourcing, channel and geo strategies. How will Central Corporate Command operate as a resource gate-keeper? Hope all involved are paying special attention to learnings from VF Corp’s new CEO.

Elevated brand positioning. Target consumer focused on tech performance and premium quality. Product offer repositioned to focus on premium items. Reduced number of entry-level price points. Crystal clear.

Strategic transformation of GTM strategy. Arc’teryx - DTC focus due to tech nature of product. Salomon - Historically wholesale driven. Focus on premium retail partners. DTC to grow with elevated investment in China. Wilson - Similar to Salomon. 50% of revenue from differentiated specialty retail.

Accelerated brand penetration in Greater China. No surprises here given the origin of investment capital circa 2019. GC is driven by a vertical retail model and Amer have been aggressively opening owned retail doors in high-traffic locations. The retail model is set-up to deliver high-end, luxury oriented in-store presentation and execution with frequent inventory refresh. They maintain a base of 21 factory retail doors (25% of fleet) to flush excess inventory. High-risk, high-reward in China these days.

Divest of brands without large market penetration and significant upside potential. Mavic (2019), Precor (2021), Suunto (2022).

Hire the right leaders to execute the transformation plan and growth strategy. Amer has reshuffled executive leadership deck across the portfolio. They’ve delivered aggressive growth in 2023 on revenue (+30%) and gross margin (+260 bps) but show mounting net losses since 2020 and significant debt. Growth isn’t free. While IPO funds will bring some financial relief; Amer execs should expect a new level of scrutiny once a publicly held company.

*Full-year revenue estimates by Footwear Insider based on published 9-month revenue and other information provided by Amer Sports.

Grab your glasses, eye chart alert. Please accept my apologies in advance if you are trying to view this on your phone. I’m learning this newsletter platform as we go.

Core brand level snapshot below

Key shifts last 5-yrs

Growth drivers

Geography mix

Distribution mix

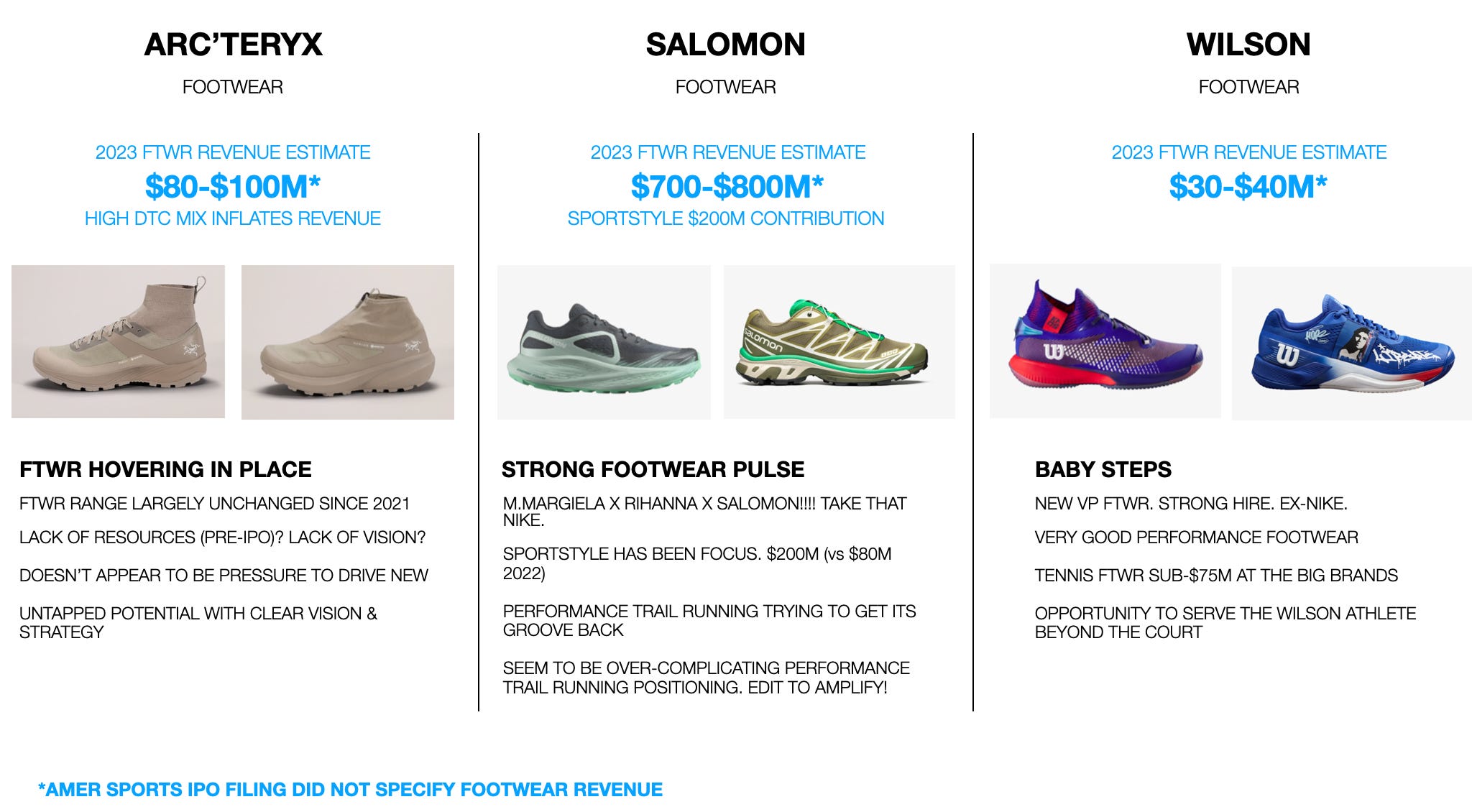

Footwear snapshot below:

*Footwear revenue estimated by Footwear Insider based on background research.

I’m going to let this post marinate for another week and then come back with more context and commentary. There’s plenty more to share on the subject.

Have a great weekend!